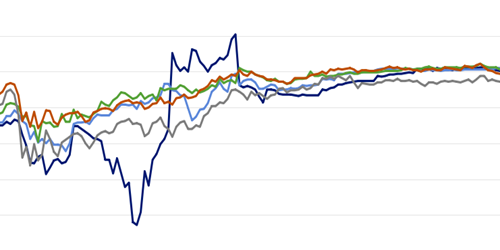

Repo Returns By Venue

Rates

Interest rates measure the cost of funding. They can act as indicators both of short-term costs of capital for financial intermediaries and of stress in funding markets. These charts present interest rates across various short-term funding markets and types of funding.

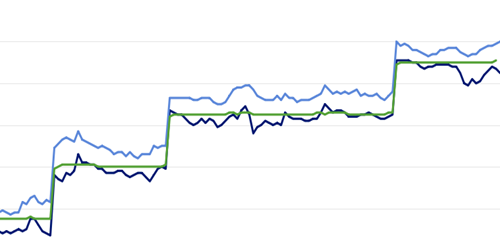

Repo returns by venue

Mean rates on repurchase agreements by venue: GCF Repo Service, DVP Service, and tri-party repo Mnemonics

Skip the ChartThe market for repurchase agreements (repo) supports short-term liquidity and price discovery by allowing financial institutions to lend or borrow cash, usually overnight, with securities as collateral. Repo venues vary on the extent to which participants know their counterparty, the extent to which they know the specific security being used as collateral, and whether their trades are cleared by a central counterparty.

The STFM currently presents data from three venues for repo transactions. The first is the tri-party market. In tri-party repurchase (repo) transactions, participants know their counterparty, but transact against classes of collateral, rather than specific securities. As a result, tri-party repo is used only for financing, and not for obtaining specific securities. A custodian, usually a bank, maintains post-trade processing activities such as collateral selection, payments and deliveries, custody of collateral securities, and collateral management.

Borrowers in tri-party tend to be larger dealers to which cash lenders are willing to be directly exposed. The Federal Reserve has used tri-party repos on occasion to deliver liquidity to dealers in times of market stress.

The second venue is the Fixed Income Clearing Corporation's (FICC) DVP Service. This is a centrally cleared market in which participants know the specific security used as collateral for a transaction. It contains both unbrokered activity, where participants know their ultimate counterparty, and brokered activity, where participants do not know their ultimate counterparty. Because DVP Service settles on a specific-security basis, some of the activity surrounds securities that lenders want, using DVP Service to gain temporary ownership of the security. Lower-than-usual rates in DVP Service relative to other venues can indicate higher-than-usual demand for specific securities, and could signal illiquidity in the cash market for securities.

The third venue is

FICC's GCF Repo Service. This is a centrally cleared market in which participants know neither the specific securities used as collateral nor their counterparty in a transaction. The venue is purely general collateral, so all activity is financing driven. Because it is counterparty-blind, it can be a popular venue for participants concerned about revealing their immediate liquidity needs.

In April 2024, additional historical data was added for DVP and GCF from May 7, 2018. Previously, data was only available from December 2019. Due to differences in the timing of data retrieval, this digest may update with a lag relative to the underlying series displayed. Transactions with the Federal Reserve and those judged to be between affiliates have been excluded from calculation of the tri-party rate.

Series Used

Related Charts

Repo returns by venue

This OFR monitor is presented solely for informative purposes and should not be relied upon for financial decisions; it is not intended to provide any investment or financial advice. If you have any specific questions about any financial or other matter please consult an appropriately qualified professional. The OFR makes no warranty, express or implied, nor assumes any legal liability or responsibility for the accuracy, completeness, reliability, and usefulness of any information that is available through this website, nor represents that its use would not infringe on any privately owned rights.

Disclaimer Regarding Non-OFR Data and InformationFor convenience and informational purposes only, the OFR may provide links and references to nongovernment sites. These sites may contain information that is copyrighted with restrictions on reuse. Permission to use copyrighted materials must be obtained from the original source and cannot be obtained from the OFR or from the U.S. Treasury Department. The OFR is not responsible for the content of external websites linked to or referenced from this site or from the OFR web server. The U.S. government, the U.S. Treasury Department, the Financial Stability Oversight Council, and the OFR neither endorse the data, information, content, materials, opinions, advice, statements, offers, products, services, presentation, or accuracy, nor make any warranty, express or implied, regarding these external websites. Please note that neither the U.S. Treasury Department nor the OFR controls, and cannot guarantee, the relevance, timeliness, or accuracy of third-party content or other materials. Users should be aware that when they select a link on this OFR website to an external website, they are leaving the OFR site.

Suggested CitationOffice of Financial Research, "OFR Short-term Funding Monitor," refreshed daily, https://www.financialresearch.gov/short-term-funding-monitor/ (accessed ).