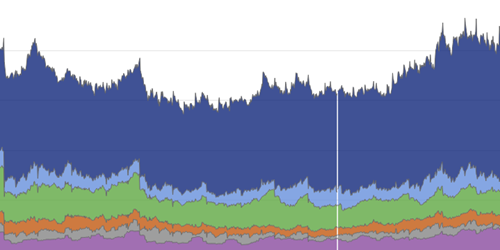

Primary Dealer Reverse Repo And Securities Borrowing By Tenor

Tenor

The tenor of a financial contract refers to the amount of time before that contract expires. Tenor aggregates can be used to examine the provision of funding over different time horizons. These charts present insights into the tenor of financing across various short-term funding markets.

Primary dealer reverse repo and securities borrowing by tenor

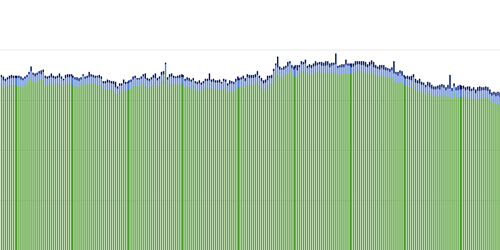

Aggregate outstanding volume in reverse repo and securities borrowing for primary dealers broken out by tenor Mnemonics

Skip the ChartPrimary dealers serve as intermediaries in securities markets, receiving securities from sellers and delivering them to buyers. They also serve a unique role in purchasing Treasury securities at auction and acting as a counterparty to the Federal Reserve. Primary dealers commonly use reverse repurchase agreements (reverse repo) to temporarily secure inventories to offer to buyers. In a reverse-repo transaction, dealers lend cash on a short-term basis while accepting securities as collateral. Securities borrowing is an alternative to reverse repo. Much as with reverse repo, in securities borrowing primary dealers borrow securities, often on a short-term basis. A key difference between securities borrowing and reverse repo is that securities borrowing contracts tend to allow lenders to recall the underlying security at will, which makes securities lending convenient for equity holders who want the option to exercise voting rights. As a result, securities borrowing tends to be

more common with equity instruments, while reverse repo tends to be more common with fixed-income instruments.

This chart shows a breakdown of primary dealer securities borrowing and reverse repo positions by tenor. Tenor is the amount of time between the initial trade of cash for securities and the repurchase of those securities. Primary dealers' financing needs can vary by time horizon, leading to demand for loans of a different tenor. Shorter-tenor trades maximize lenders' liquidity, typically reducing rates primary dealers have to pay. However, when primary dealers borrow in shorter-tenor trades they carry the risk that financing rates increase or that financing becomes unavailable, which is referred to as rollover risk. In addition, longer-tenor trades are treated differently for regulatory purposes than shorter-tenor trades. Examining volume across tenors for primary dealers provides a window into the availability of and demand for financing across time horizons. In periods of

high volatility, longer-tenor trades can provide more stability to borrowers, but during these times it may also be difficult for lenders to extend credit at longer horizons.

Series Used

Related Charts

Centrally cleared repo outstanding volume by venue and tenor

This OFR monitor is presented solely for informative purposes and should not be relied upon for financial decisions; it is not intended to provide any investment or financial advice. If you have any specific questions about any financial or other matter please consult an appropriately qualified professional. The OFR makes no warranty, express or implied, nor assumes any legal liability or responsibility for the accuracy, completeness, reliability, and usefulness of any information that is available through this website, nor represents that its use would not infringe on any privately owned rights.

Disclaimer Regarding Non-OFR Data and InformationFor convenience and informational purposes only, the OFR may provide links and references to nongovernment sites. These sites may contain information that is copyrighted with restrictions on reuse. Permission to use copyrighted materials must be obtained from the original source and cannot be obtained from the OFR or from the U.S. Treasury Department. The OFR is not responsible for the content of external websites linked to or referenced from this site or from the OFR web server. The U.S. government, the U.S. Treasury Department, the Financial Stability Oversight Council, and the OFR neither endorse the data, information, content, materials, opinions, advice, statements, offers, products, services, presentation, or accuracy, nor make any warranty, express or implied, regarding these external websites. Please note that neither the U.S. Treasury Department nor the OFR controls, and cannot guarantee, the relevance, timeliness, or accuracy of third-party content or other materials. Users should be aware that when they select a link on this OFR website to an external website, they are leaving the OFR site.

Suggested CitationOffice of Financial Research, "OFR Short-term Funding Monitor," refreshed daily, https://www.financialresearch.gov/short-term-funding-monitor/ (accessed ).