Hedge Funds and Treasury Market Price Impact: Evidence from Direct Exposures

Published: August 23, 2022

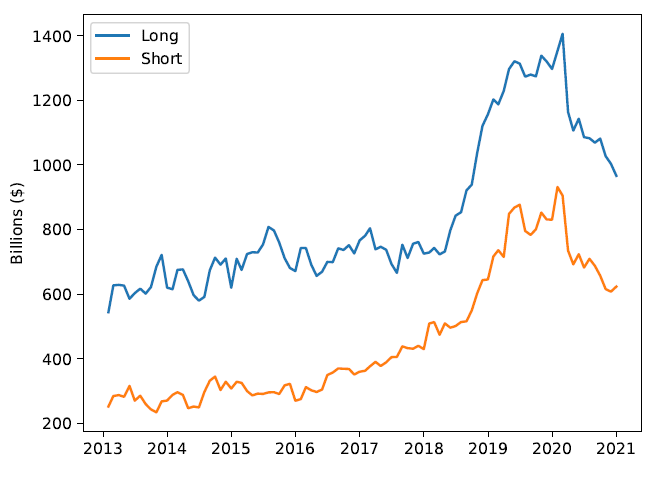

The increasing importance of non-bank financial intermediaries has raised new questions about the risks that hedge funds pose to the financial system. The OFR examined how changes in hedge fund exposures affect U.S. Treasury prices and the yield curve. Using confidential hedge fund data from the SEC’s Form Private Fund (PF), OFR analysts calculated hedge funds’ aggregate, net Treasury exposures, and their fluctuations over time. This revealed economically significant and consistent evidence that changes in hedge fund exposures are related to Treasury yield changes. Furthermore, particular strategy groups and lower-levered hedge funds were seen to have a larger estimated price impact on Treasuries. Finally, asset pricing tests show that U.S. Treasury investors demand additional return compensation due to the risks associated with hedge fund demand (Working Paper no. 22-05).

Abstract

Financial intermediaries play a key role in the formation of asset prices. More specifically, the increasing importance of non-bank financial intermediaries has raised new questions about the risks that hedge funds pose to the financial system. We focus on the role that changes in hedge fund exposures play in driving U.S. Treasury prices and the yield curve. Using confidential hedge-fund data from the SEC’s Form Private Fund (PF), we calculate hedge funds’ aggregate, net Treasury exposures, and their fluctuations over time. We find economically significant and consistent evidence that changes in aggregate hedge fund exposures are related to Treasury yield changes. In the cross-section of hedge funds, we also show that particular strategy groups and lower-levered hedge funds display a larger estimated price impact on Treasuries. Finally, asset pricing tests show evidence of positive risk compensation associated with shifts in hedge fund Treasury demand.

Keywords: Hedge funds; price impact; U.S. Treasury market.

JEL Classifications: E43, G12, G20, G23