Anatomy of the Repo Rate Spikes in September 2019

Published: April 25, 2023

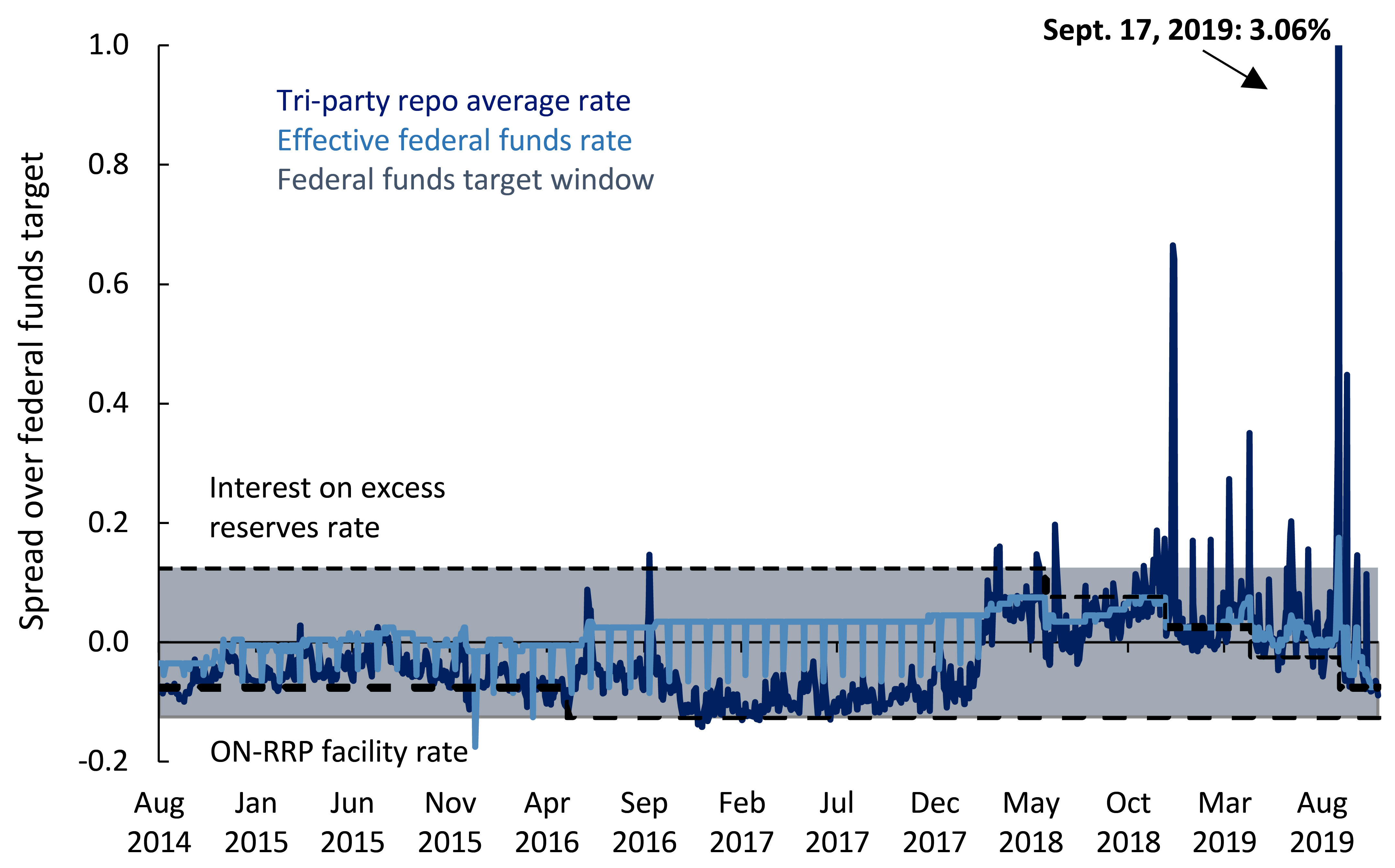

Repurchase agreement (repo) markets represent one of the largest sources of funding and risk transformation in the U.S. financial system. Despite the large volume, repo rates can be quite volatile, and in the extreme, they have exhibited intraday spikes that are 5-10 times the rate on a typical day. This paper uses a unique combination of intraday timing data from the repo market to examine the potential causes of the dramatic spike in repo rates in mid-September 2019 (Working Paper no. 23-04).

Abstract

Repurchase agreement (repo) markets represent one of the largest sources of funding and risk transformation in the U.S. financial system. Despite the large volume, repo rates can be quite volatile, and in the extreme, they have exhibited intraday spikes that are 5-10 times the rate on a typical day. This paper uses a unique combination of intraday timing data from the repo market to examine the potential causes of the dramatic spike in repo rates in mid-September 2019. We conclude that the spike resulted from a confluence of factors that, when taken individually, would not have been nearly as disruptive. Our work highlights how a lack of information transmission across repo segments and internal frictions within banks most likely exacerbated the spike. These findings are instructive in the context of repo market liquidity, demonstrating how the segmented structure of the market can contribute to its fragility.

Keywords: Repurchase agreements, financial intermediation, market segmentation, short-term funding, rate spikes.

JEL Classifications: G14, D40, D82