The Effects of the Volcker Rule on Corporate Bond Trading: Evidence from the Underwriting Exemption

Published: August 6, 2019

This paper examines the impact of the Volcker rule, which bans proprietary trading by commercial banks and their affiliates, with some exceptions. It finds evidence that the rule has increased the cost of liquidity provided by firms it covers, but not decreased the firms’ exposure to liquidity risk. It also finds that the rule has decreased the market share of covered firms. Customers appear to be trading more with non-bank dealers, who are exempt from the Volcker rule but also cannot borrow at the Federal Reserve’s discount window. (Working Paper no. 19-02)

Abstract

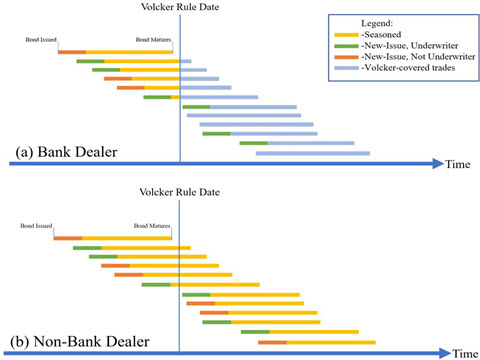

Using a novel within-dealer, within-security identification strategy, we examine intended and unintended effects of the Volcker rule on covered firms’ corporate bond trading using dealer-identified regulatory data. We use the underwriting exemption to isolate the Volcker rule’s effects separate from other post-crisis changes in bank regulation and broader trends in market liquidity. We find no evidence of the rule’s intended reduction in the riskiness of covered firms’ trading in corporate bonds. We find significant adverse liquidity effects on covered firms’ corporate bond trading with 20-45 basis points higher costs for customers even for roundtrip trades of shorter duration. These effects do not appear to be transitional. The Volcker rule appears to have increased the cost of the liquidity provided by covered firms and has not decreased the liquidity risk exposure of covered firms. Finally, the Volcker rule has decreased the market share of covered firms. Customers appear to be trading more with non-bank dealers, who are exempt from the Volcker rule but also lack access to emergency liquidity support at the Fed’s discount window.