CoCos, Bail-in, and Tail Risk

Published: January 23, 2013

This paper develops a capital structure model of a bank to analyze the incentives created by contingent convertibles (CoCos) and bail-in debt, which convert to equity when a bank approaches insolvency. These two forms of contingent capital have been proposed as potential mechanisms to enhance financial stability. (Working Paper no. 13-04)

Abstract

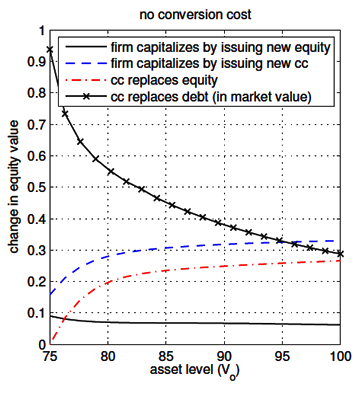

Contingent convertibles (CoCos) and bail-in debt for banks have been proposed as potential mechanisms to enhance financial stability. They function by converting to equity when a bank approaches insolvency. We develop a capital structure model to analyze the incentives created by these forms of contingent capital. Our formulation includes firm-specific and market-wide tail risk in the form of two types of jumps and leads to a tractable jump-diffusion model of the firm’s income and asset value. The firm’s liabilities include insured deposits and senior and subordinated debt, as well as convertible debt. Our model combines endogenous default, debt rollover, and jumps; these features are essential in examining how changes in capital structure to include CoCos or bail-in debt change incentives for equity holders. We derive closed-form expressions to value the firm and its liabilities, and we use these to investigate how CoCos affect debt overhang, asset substitution, the firm’s ability to absorb losses, the sensitivity of equity holders to various types of risk, and how these properties interact with the firm’s debt maturity profile, the tax treatment of CoCo coupons, and the pricing of deposit insurance. We examine the effects of varying the two main design features of CoCos, the conversion trigger and the conversion ratio, and we compare the effects of CoCos with the effects of reduced bankruptcy costs through orderly resolution. Across a wide set of considerations, we find that CoCos generally have positive incentive effects when the conversion trigger is not set too low. The need to roll over debt, the debt tax shield, and tail risk in the firm’s income and asset value have particular impact on the effects of CoCos. We also identify a phenomenon of debt-induced collapse that occurs when a firm issues CoCos and then takes on excessive additional debt: the added debt burden can induce equity holders to raise their default barrier above the conversion trigger, effectively changing CoCos to junior straight debt; equity value experiences a sudden drop at the point at which this occurs. Finally, we calibrate the model to past data on the largest U.S. bank holding companies to see what impact CoCos might have had on the financial crisis. We use the calibration to gauge the increase in loss absorbing capacity and the reduction in debt overhang costs resulting from CoCos. We also time approximate conversion dates for high and low conversion triggers.