Risk Spotlight: OFR Identifies Three Ways DeFi Growth Could Threaten Financial Stability

Published: February 7, 2023

Views and opinions expressed are those of the authors and do not necessarily represent official positions or policy of the OFR or Treasury.

If decentralized finance (DeFi) continues to grow in size and scope, and if it continues to lack the guardrails that exist for traditional finance, then it could become a threat to financial stability. This blog post summarizes three channels through which threats could emerge in the DeFi market. More information can be found in the OFR’s 2022 Annual Report to Congress.

1. Effects from Price Declines of Digital Assets Could Spill Over into Traditional Financial Markets

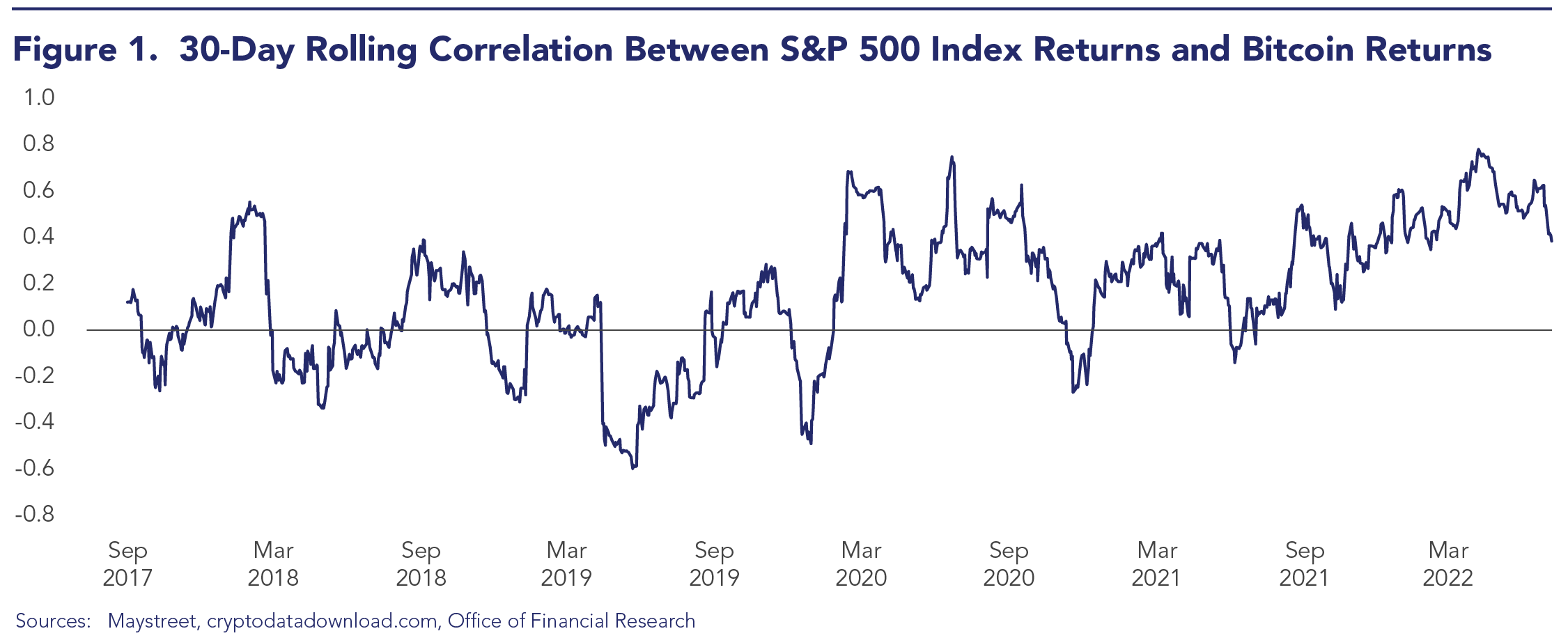

If traditional financial market participants and institutions accumulate significant exposure to digital assets, then future price declines in or disruptions of the digital-assets market could have spillover effects in traditional financial markets and the real economy. Reports indicate that a majority of the world’s largest banks have already invested in companies operating in the digital-asset or blockchain-related space, to some degree.1 However, this information is primarily based on press releases from the banks or companies involved. Regulatory data on the exposures of traditional institutions to crypto assets are currently scarce, making it difficult to monitor the interconnectedness of crypto assets and traditional financial markets. Some indirect evidence of this interconnectedness can be gleaned from return correlations. For example, the 30-day rolling correlation between the returns on Bitcoin and the S&P 500 has increased noticeably since the beginning of 2021.

2. Rapid Withdrawals of Digital Assets Could Create Losses for Traditional Financial Institutions

Decentralized finance could create financial-stability risks through its direct integration with the real economy. Currently, most activity in decentralized finance supports trading and speculation in digital assets. However, an important exception involves non-crypto assets, including commercial paper, that purportedly back some stablecoins. Especially if stablecoins continue to grow, rapid withdrawals from stablecoins backed by commercial paper could potentially disrupt commercial-paper markets. This would create losses for traditional financial institutions holding similar assets and disrupt financing for commercial-paper issuers. This risk could increase further if traditional borrowers were to obtain funding through stablecoins or crypto asset lenders. Regulatory data on the assets held by such lenders would be an essential input to monitoring this risk.

3. Disruptions Would Have Immediate Consequences If Digital Assets Were Widely Used as Payment

Digital assets could become a threat to financial stability if they were widely adopted as a means of payment. While volatile crypto assets like Bitcoin are unlikely to become a means of payment, stablecoins are expressly designed to serve this purpose for blockchain-based transactions. Proponents claim that blockchain technology may be adopted for various commercial uses over time, such as tracking and verifying components in global supply chains. A blockchain-native means of payment, such as a worldwide stablecoin, could bring substantial efficiencies to such processes. If market participants were to adopt such a stablecoin, disruption or failure in the stablecoin market could have immediate economic consequences.

Digital assets and decentralized finance generally remain small parts of the overall financial system, with limited linkages to other financial markets and the real economy. For these reasons, the current risks to financial stability from these new financial arrangements remain modest. However, past periods of rapid growth suggest that, under the right conditions, a shift from low to high risk from DeFi could happen quickly. Therefore, developments in this market should continue to be monitored to identify emerging risks.

1Team Blockdata. 2022. “Top Banks Investing in Crypto and Blockchain May 2022 Update.” Blockdata (June 14, 2022). https://www.blockdata.tech/blog/general/top-banks-investing-in-crypto-and-blockchain-may-2022-update.