Technology Shocks and Predictable Minsky Cycles

Published: June 12, 2023

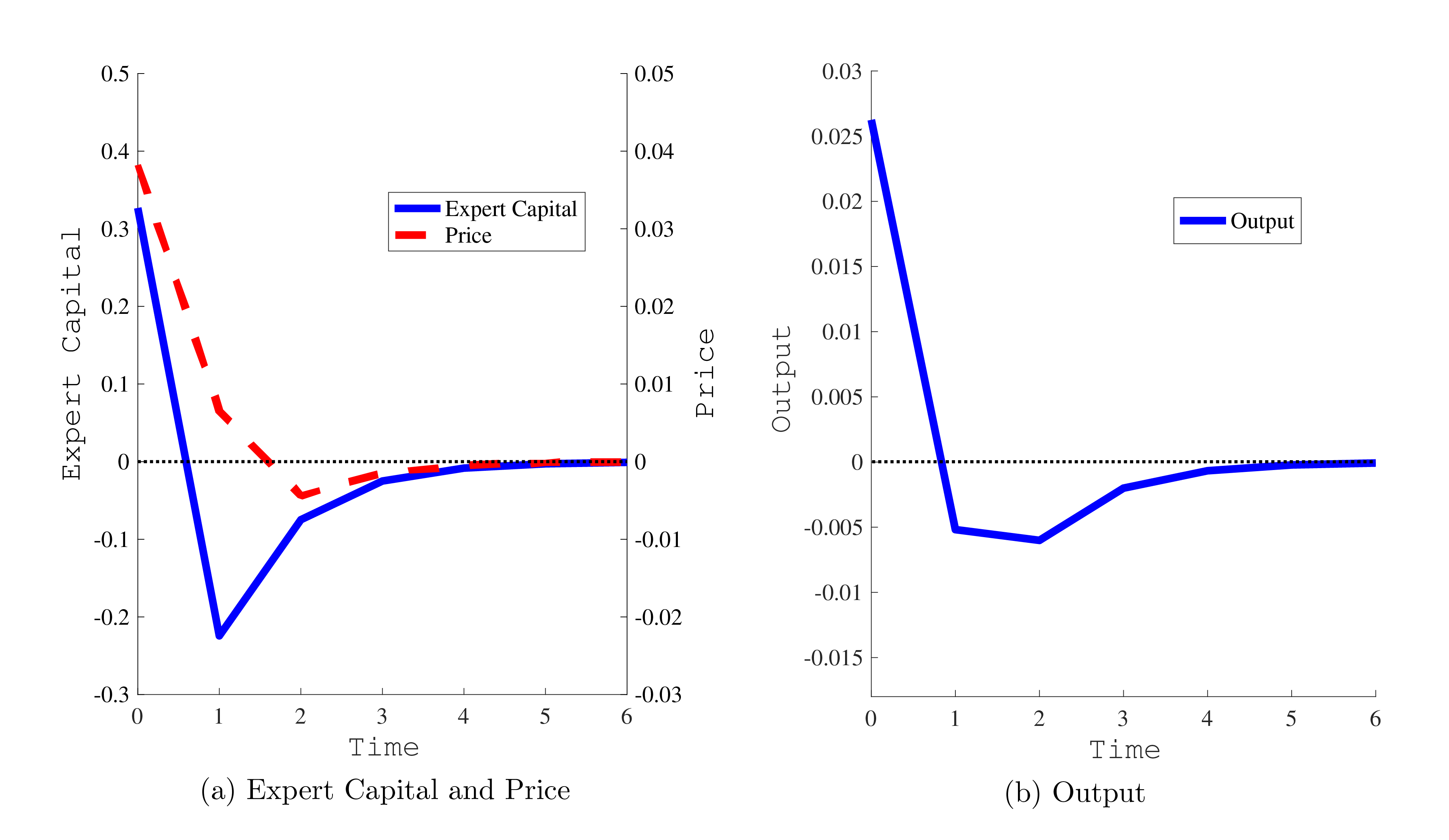

This paper offers an economical and internally consistent model to rationalize macrofinancial boom-bust cycles. The authors present a simple model that can clarify the interaction of optimism with capital reallocation and demonstrate how this interaction can generate predictable boom-bust financial cycles. This clarification enhances our understanding of the channels through which credit markets could threaten financial stability. The model is also a starting point for future research that could have important implications for welfare and policy. Adding more features to the model could help identify optimal policy responses to mitigate the boom’s initial size and thus mitigate the bust’s size (Working Paper no. 23-06).

Abstract

Big technological improvements in a new, secondary sector lead to a period of excitement about the future prospects of the overall economy, generating boom-bust dynamics that propagate through credit markets. Increased future capital prices relax collateral constraints today, leading to a boom before the realization of the shock. But reallocation of capital toward the secondary sector when the shock hits leads to a bust going forward. These cycles are perfectly foreseen in our model, making them markedly different from the typical narrative about unexpected financial shocks that is used to explain crises. In fact, these cycles echo Minsky’s original narrative for financial cycles, according to which, “financial trauma occur as normal functioning events in a capitalistic economy.”

Keywords: cyclical propagation, endogenous cycles, boom-bust dynamics, optimism, credit markets, predictability

JEL Classifications: : E22, E23, E32, E44