Financial Intermediary Funding Constraints and Segmented Markets

Published: February 10, 2022

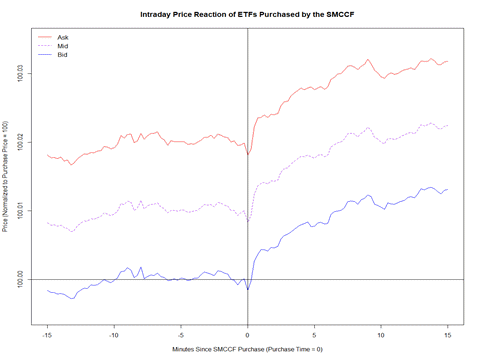

This working paper examines the role of financial intermediaries, namely authorized participants (APs), in the propagation of shocks across funds that they support and the underlying assets held by those funds. Corporate bond ETF trades by the Federal Reserve through the Secondary Market Corporate Credit Facility (SMCCF) beginning in May 2020 were extremely large and likely alleviated inventory capacity constraints for APs that were counterparties to those transactions. ETFs that were not traded by the Federal Reserve, but overlap in their bond holdings with those traded, exhibit a positive and significant price reaction within minutes of the transaction. Consistent evidence is found for the prices of their underlying bonds. The paper’s findings support the view that the inclusion of ETFs in the SMCCF had broader “spillover” effects in stabilizing markets beyond the ETFs directly targeted by the program (Working Paper no. 22-01).

Abstract

This paper examines a quasi-natural experiment to study the effect of balance sheet frictions among financial intermediaries on the pricing and liquidity of segmented asset markets. Corporate bond ETF purchases by the Federal Reserve through the Secondary Market Corporate Credit Facility (SMCCF) beginning in May 2020 were extremely large, likely alleviating inventory capacity constraints for authorized participants (APs) who were counterparties to those transactions. Other ETFs not purchased by the Fed—but overlap in their underlying bond holdings with purchased ETFs—exhibit significant positive price reaction within seconds of the transaction. Bonds held by ETFs purchased by the Fed also exhibit a significant and positive price reaction as well as improved liquidity on the day of the transaction. We offer additional evidence that these reactions reflected the effects of the purchases on AP balance sheet liquidity. The paper’s findings support the view that the inclusion of ETFs in the SMCCF had broader “spillover” effects in stabilizing markets beyond the ETFs directly targeted by the program. More broadly, our paper provides strong evidence that the “health” of financial intermediaries has important implications for the liquidity and prices of the securities that they trade.

Keywords: Financial intermediaries, authorized participants, corporate bond ETFs, corporate bonds, Covid-19, Federal Reserve, regulatory interventions.

JEL Classifications: G12, G14, G23