Are the Borrowing Costs of Large Financial Firms Unusual?

Published: May 13, 2015

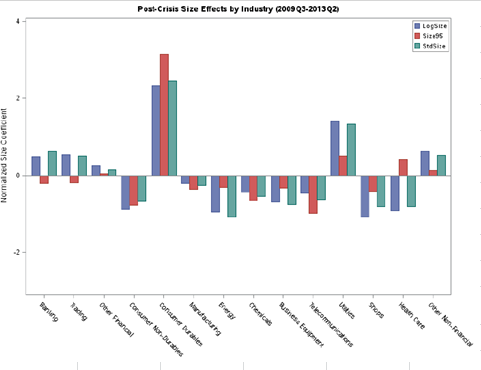

This paper examines evidence of a too-big-to-fail subsidy for large financial firms by comparing borrowing costs of large and small firms across industries. The paper finds that larger firms borrow more cheaply in many industries, and this size effect is often largest in nonfinancial industries. These results challenge the notion that expected government bailouts are behind borrowing cost advantages enjoyed by the largest financial firms. (Working Paper no. 15-10)

Abstract

Expectations of government support for large financial firms are often based on their lower borrowing costs relative to smaller financial firms. However, large financial firms are not unique in this regard: larger firms enjoy lower borrowing costs in several industries. We show that size-related borrowing cost advantages are not unusually large in the financial industry, and spreads are actually more sensitive to borrower size in several nonfinancial industries. These size-related differences are not explained by differences in risk and are only partially explained by higher liquidity and recovery rates for larger borrowers. Our results suggest that estimates of implicit government guarantees for financial firms may overemphasize the relationship between size-related borrowing cost differentials and expected bailouts. Our analysis also suggests that in the period leading to the 2008-9 financial crisis, perceptions of reduced risk may have lowered borrowing costs for the financial industry as a whole.

Keywords: Financial industry, too-big-to-fail, implicit government guarantee, size effect, borrowing costs, credit default swaps JEL classification: G21, G22, G24, G28