The Effect of Negative Equity on Mortgage Default: Evidence from HAMP PRA

Published: May 7, 2015

This paper uses data from the Home Affordable Modification Program to examine the impact of principal forgiveness on mortgage default. On average 3.1 percent of loans become delinquent and exit the program each quarter. The authors estimate that the rate would have been 3.8 percent absent principal forgiveness, which averaged 28 percent of the initial mortgage balance. (Working Paper no. 15-06)

Abstract

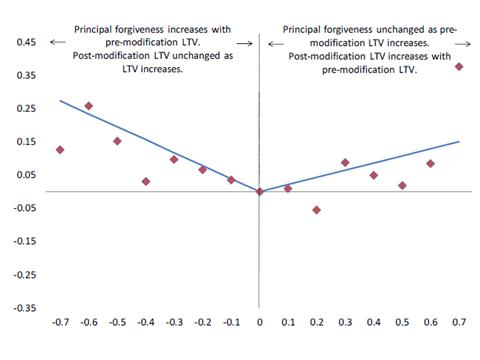

The Home Affordable Modification Program’s Principal Reduction Alternative (HAMP PRA) is a government-sponsored program to reduce the principal balances and monthly mortgage payments of borrowers with negative equity (mortgage balances in excess of their home value, or “under water”) who are in danger of default. We use administrative data to examine the impact of principal forgiveness — a permanent mortgage balance reduction — on borrowers’ subsequent mortgage default. The program’s rules imply a kink in the relationship between principal forgiveness and a borrower’s initial equity level ceteris paribus. Our identification strategy exploits the quasi-experimental variation in principal forgiveness generated by this kink using a regression kink design (RKD), which compares the relationship between initial equity and default on either side of the kink. The quarterly hazard — the proportion of loans that become more than 90 days delinquent and consequently exit the program — in our sample is 3.1 percent; we estimate that it would have been 3.8 percent absent principal forgiveness, which averaged 28 percent of the initial mortgage balance.

JEL Codes: G21 (Mortgages), R30 (Real Estate Markets, General)