Shadow Banking: The Money View

Published: July 2, 2014

This paper presents an accounting framework for measuring the sources and uses of short-term funding in the global financial system and introduces a dynamic map of global funding flows. (Working Paper no. 14-04)

Abstract

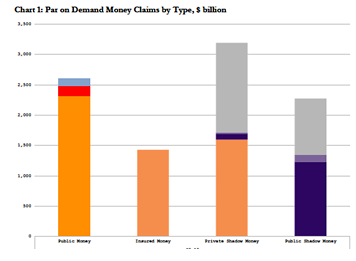

This paper presents an accounting framework for measuring the sources and uses of short-term funding in the global financial ecosystem. We introduce a dynamic map of global funding flows to show how dealer banks emerged as intermediaries between two types of asset managers: cash pools searching for safety via collateralized cash investments and levered portfolio managers searching for yield via funded securities portfolios and derivatives. We argue that the monetary aggregates (M0, M1, M2, etc.) and the Financial Accounts of the United States (formerly the Flow of Funds) do not adequately reflect the institutional realities of the modern financial ecosystem, and should be updated to allow policymakers to better analyze and monitor the shadow banking system and its potential contributions to financial instability. The monetary aggregates, used mainly to inform the aggregate demand management aspects of monetary policy, do not include the instruments that asset managers use as money, particularly repos. Asset managers’ money demand is not driven by transaction needs in the real economy but in the financial economy: in this sense, repo-based money dealing activities in the shadow banking system are about the provision of working capital for asset managers, much like real bills provided working capital for merchants and manufacturers in Bagehot’s world over 150 years ago. These developments should be systematically captured in a new set of Flow of Collateral, Flow of Risk and Flow of Eurodollar satellite accounts to supplement the Financial Accounts. The accounting framework presented with this paper also explains how the Federal Reserve’s reverse repo facility helps reduce interconnections within the financial system and how they could evolve into minimum liquidity requirements for shadow banks and a tool to control market-based credit cycles. The global macro drivers behind the secular rise of cash pools and leveraged portfolio managers in the asset management complex are identical with the real economy drivers behind the idea of secular stagnation. As such, one way to interpret shadow banking is as the financial economy reflection of real economy imbalances caused by excess global savings, slowing potential growth, and the rising share of corporate profits relative to wages in national income.

Attachment: