How Well Will a Central Counterparty Withstand Severe Credit Stress?

Published: November 2, 2017

Many derivatives trades that would have been conducted directly between the buyer and seller before the financial crisis now go through central counterparties (CCPs). Reforms after the financial crisis promoted the use of CCPs. This arrangement improves transparency and reduces counterparty risk, as long as market participants manage that risk properly. If they don’t, a CCP’s links to member firms could increase systemic risk.

An OFR working paper released today describes a new way to estimate how likely a CCP is to default under severe stress. The research underlying this paper contributes to the broader trend in CCP stress testing that considers implications beyond the default of an individual CCP’s two largest clearing members — known as the “cover 2” standard. (Most CCP members are bank holding companies that clear on behalf of their clients.)

The Commodity Futures Trading Commission (CFTC), the U.S. regulator responsible for overseeing CCPs, has also started going beyond the cover 2 approach to look at systemic effects of a default by a clearing member. Its most recent stress test, released last month, considered a shock to clearing members and their clients that would affect all CCPs simultaneously. Using the CFTC’s methodology and stress scenario, the three leading CCPs would have sufficient liquidity to meet their payment obligations.

The OFR working paper takes a macroprudential approach to evaluating the systemic effects of a CCP default. In the paper, “How Safe are Central Counterparties in Derivatives Markets?”, authors Mark Paddrik and Peyton Young of the OFR consider the effects of contagion on a CCP’s network of client firms and clearing members.

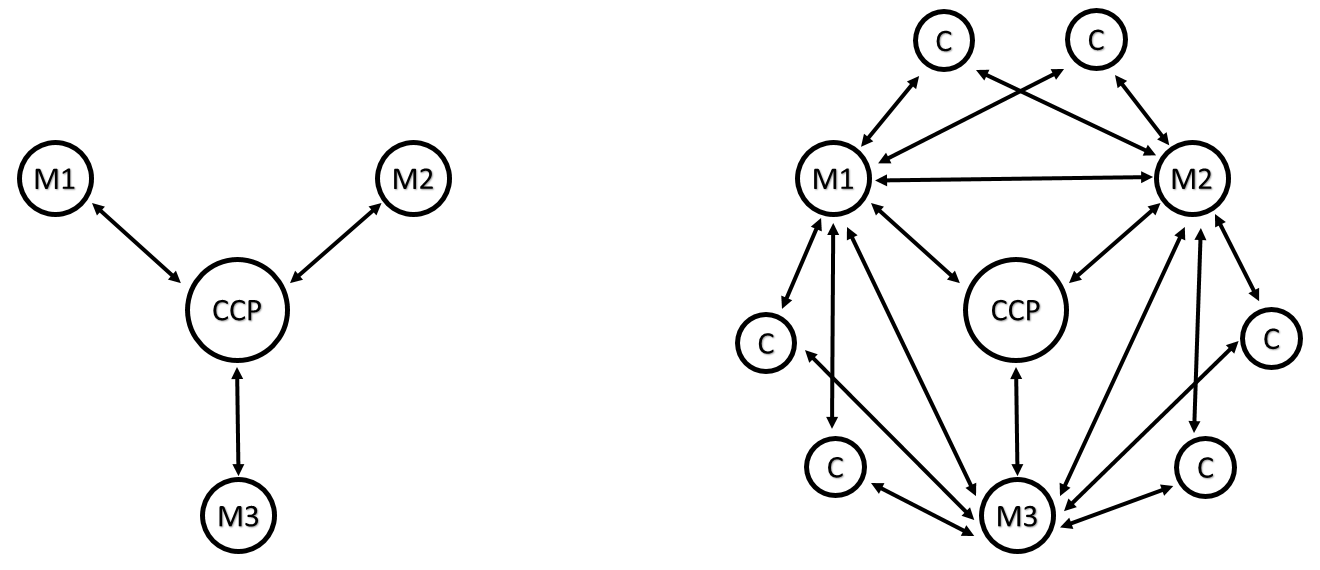

An illustration from the paper shows how financial contagion can spread in a CCP network. In Figure 1, the left panel shows the direct exposure of three members to a CCP. The right panel shows the network of exposures among members. Suppose two of the three members (M1 and M2) default on their payments. If M1 and M2 owe money to nonmember clients C, the nonmember clients may be unable to meet margin calls to their counterparties, which may include M3. This spillover could cause M3 to fail, which may lead to default by the CCP.

Figure 1. Network Depiction of CCP Stress Testing and Spillover Effects

Note: M = member, C = client

Source: Paddrik and Young (2017)

The researchers demonstrate their approach using confidential data from the credit default swap market. They use network analysis to estimate total payment shortfalls from a potential financial shock similar to the scenarios in the Federal Reserve’s 2015 bank stress tests. Their analysis shows that under the 2015 shock conditions, the main CCP for the credit default swap market is not likely to fail from contagion effects. Under more severe shocks, however, the CCP could be more likely to fail than the average CCP member.

The cover 2 standard does not account for this type of indirect network contagion among client firms, member firms, and the CCP. Although most firms are not directly exposed to a CCP, a failure by any of them could cascade through the network and cause members to default on their payments to a CCP. In the future, data from swap data repositories could be used to conduct further stress tests on swap markets.

The OFR has a statutory mandate to review stress tests and how they can promote financial stability. Earlier OFR work by the authors showed that during times of stress, many CCP members and clients are more likely to be sources of contagion than the CCP itself. An OFR brief published earlier this year proposed a framework that would use existing stress test results at individual CCPs to create a U.S. systemwide stress test.

Stacey Schreft is the Deputy Director for Research and Analysis at the Office of Financial Research