Measuring Systemwide Resilience of Central Counterparties

Published: February 22, 2017

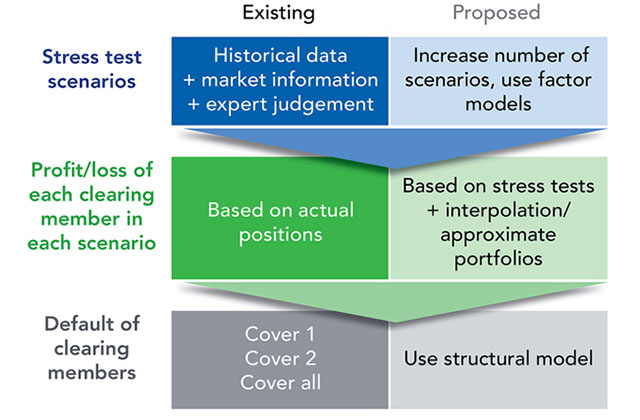

This brief proposes a novel way to conduct a U.S. systemwide stress test of central counterparties, or CCPs. The approach takes into account the impacts of losses and defaults at CCPs’ member banks. It would require little extra effort by companies because regulators can use the results of existing stress tests of CCPs. (Brief no. 17-03)